Against the backdrop of increasingly stringent environmental regulations, surging industrial electricity costs, and the urgent need for critical mineral autonomy, the conversion from alternating current (AC) to direct current (DC) equipment—especially in core metallurgical fields such as ferroalloy production, steelmaking, and hazardous waste treatment—has emerged as an inevitable trend in the U.S. industrial upgrading. Leveraging its unique advantages in energy efficiency, environmental compliance, and raw material adaptability, AC to DC conversion perfectly aligns with the U.S. government’s strategic goals of “cost reduction, decarbonization, and supply chain security,” as well as the operational demands of domestic enterprises. With strong policy support, huge market demand, and mature technical guarantees, AC to DC conversion in the U.S. boasts broad development prospects and is poised to become a key driver of the country’s industrial transformation.

1. Policy Empowerment: Creating a Favorable Environment for AC to DC Conversion

U.S. federal and state governments have introduced a series of policies to encourage industrial energy conservation, decarbonization, and technological upgrading, providing strong policy support for the promotion of AC to DC conversion. At the federal level, the Inflation Reduction Act (IRA) offers 10% tax credits for investments in advanced manufacturing equipment, covering AC to DC conversion projects for ferroalloy and steel production lines, effectively reducing the initial investment burden for enterprises. The U.S. Department of Energy (DOE) has also launched industrial efficiency and decarbonization grant programs, with 50% cost sharing available for technologies that reduce process emissions by more than 30%—a threshold easily met by DC equipment such as YND’s DC Submerged Arc Furnace.

At the regional level, increasingly stringent environmental regulations have become a direct driver for AC to DC conversion. California’s AB32 Carbon Neutrality Act, the Electric Reliability Council of Texas (ERCOT) rules, and the EPA’s 2026 Hazardous Waste Permit New Regulations have raised the bar for industrial emissions and energy efficiency. Traditional AC furnaces, characterized by high energy consumption, high electrode loss, and poor emission control, can no longer meet these new requirements, forcing enterprises to upgrade to DC equipment to avoid daily non-compliance fines of up to $250,000. Additionally, Congress is exploring ways to support high-voltage direct current (HVDC) technology, including enabling DC equipment operators to qualify for grid ancillary service payments and facilitating the construction of interregional DC transmission facilities, further laying the foundation for AC to DC conversion penetration.

2. Market Demand: Huge Stock Conversion Space Driven by Pain Points

The U.S. metallurgical industry, including ferroalloy production, steelmaking, and hazardous waste treatment, has a large stock of aging AC equipment, creating enormous market space for AC to DC conversion. Most of the existing AC submerged arc furnaces and electric arc furnaces in the U.S. have been in operation for decades, with outdated technology, low energy efficiency, and high maintenance costs—problems exacerbated by the country’s aging power infrastructure, where the average service life of electrical equipment exceeds 30 years. For example, the U.S. steel industry relies heavily on scrap-based steelmaking (scrap accounts for 51% of total steel production), and over 70% of crude steel is produced by electric arc furnaces, most of which are traditional AC models with high energy consumption.

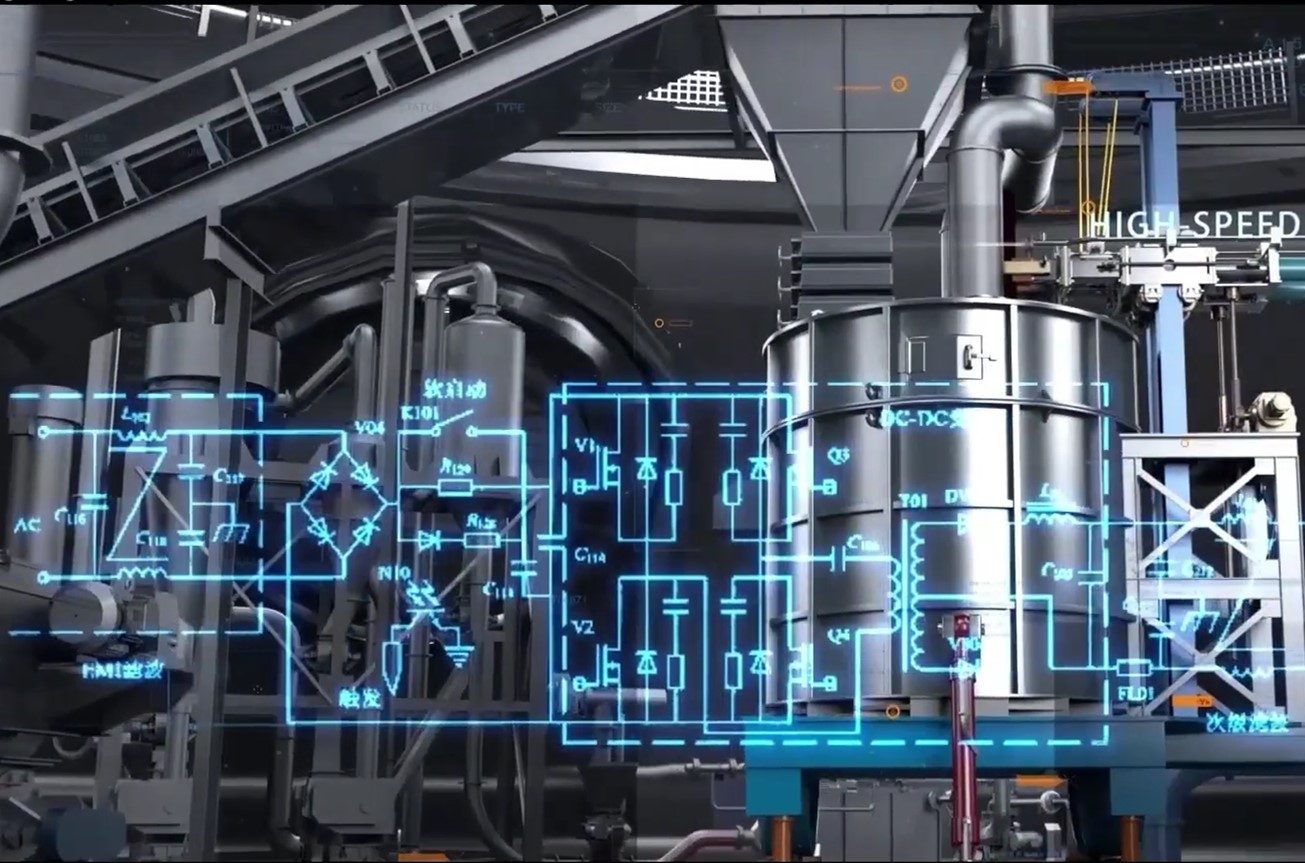

The surging U.S. industrial electricity prices have further amplified the demand for AC to DC conversion. Industrial electricity rates in the U.S. increased by 12% year-on-year in 2025, and in many states, industrial electricity prices reach $65-$82 per MWh—far higher than the affordable threshold for energy-intensive industries such as metallurgy. Electricity accounts for nearly 40% of the total production cost in energy-intensive sectors like aluminum smelting, and the proportion is similar for ferroalloy and steel production. DC equipment, which reduces energy consumption by more than 20% and electrode consumption by 35% compared to AC equipment, can significantly cut electricity and operational costs for enterprises, making AC to DC conversion a cost-effective choice to cope with high electricity prices. Practical cases such as Primetals Technologies’ successful upgrade of 16 sets of DC drive systems for Sterling Steel also demonstrate the maturity and market acceptance of AC to DC conversion technology in the U.S.industrial sector.

3. Core Drivers: Energy Conservation, Environmental Compliance and Strategic Adaptation

The broad prospects of AC to DC conversion in the U.S. are fundamentally driven by three core demands: energy conservation and cost reduction, environmental compliance, and strategic mineral autonomy. Firstly, in terms of energy conservation and cost reduction, DC equipment’s superior energy efficiency directly addresses the pain point of high operational costs for U.S. enterprises. Taking a 1 million-ton capacity ferroalloy production line as an example, AC to DC conversion can save enterprises $2.8-$3.5 million annually in electricity costs and $1.5-$2.2 million in electrode costs, with a payback period of 2-3 years, creating significant economic benefits.

Secondly, in terms of environmental compliance, DC equipment’s hermetically sealed design and high-efficiency flue gas capture system can reduce dust emissions by 40% and achieve 100% harmless conversion of hazardous waste, fully meeting EPA’s MACT standards and regional environmental regulations. This helps enterprises avoid huge non-compliance fines and reduce environmental upgrade costs by 40%, while also aligning with the U.S. industrial electrification and decarbonization goals—industrial electrification combined with a clean grid is expected to reduce U.S. industrial greenhouse gas emissions by 19%-26% by 2050. Thirdly, in terms of strategic adaptation, DC equipment’s strong raw material adaptability allows it to efficiently process low-grade ores such as Minnesota iron concentrate and Michigan nickel-cobalt ore without fine beneficiation pretreatment, helping the U.S. reduce its 90% dependence on imported high-end ferroalloys and promote the localization of critical mineral supply chains, which is in line with the goals of the Defense Production Act and IRA.

4. Implementation Guarantees and Potential Challenges

The mature technical solutions and localized services have laid a solid foundation for the large-scale promotion of AC to DC conversion in the U.S. Technologies such as minimally invasive retrofitting can complete AC to DC conversion within 7-15 days with an investment 30%-50% lower than purchasing new equipment, minimizing the impact of production shutdowns on enterprises. Localized service systems, including on-site installation, commissioning, and after-sales support, have also eliminated U.S. enterprises’ concerns about imported technology and after-sales risks.

However, AC to DC conversion in the U.S. also faces certain potential challenges: the initial investment in conversion is relatively high, which may bring financial pressure to small and medium-sized enterprises; the shortage of professional technical talents in some regions may affect the speed of conversion promotion; and the aging U.S. power grid may face adaptation challenges when integrating a large number of DC equipment. Nevertheless, these challenges can be gradually resolved with the support of government subsidies, the cultivation of localized technical teams, and the upgrading of grid infrastructure—Congress is already promoting the improvement of the grid interconnection process and supporting the construction of DC transmission facilities on federal land to address these issues.